By Leela Vosko, Director of Impact

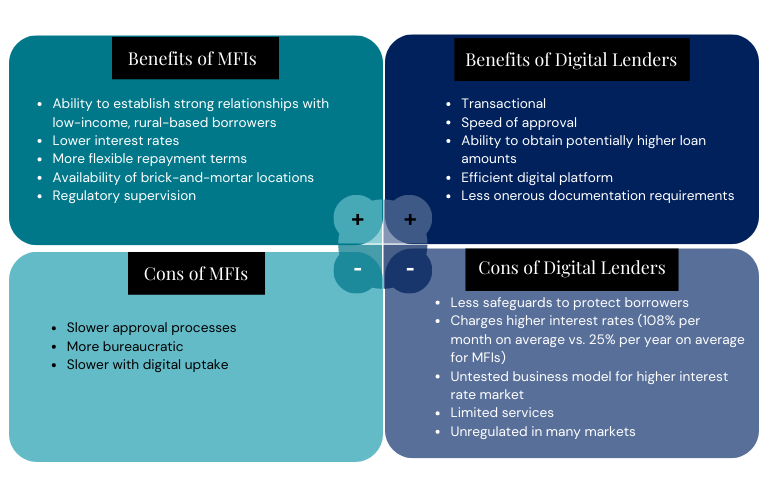

Over the past several decades, micro and small and medium-sized enterprise (SME) financial institutions (MFIs) have demonstrated their ability to establish strong, long-term relationships with low-income borrowers while achieving low default rates through robust underwriting methodology. Being deeply rooted in their communities, MFIs operate within a pre-existing regulatory framework and have strong incentives to work with customers over long periods who may require more flexible repayment terms. Their traditional “brick and mortar” presence enables them to offer a wider range of banking services beyond lending and serves as a platform for launching digital financial services.

In recent years, digital financial services platforms, or Fintechs, have also brought basic banking services, payments, and lending to many emerging and frontier markets. Fintech is as much a set of tools and methods as it is a distinct type of company. Many of the best MFIs are utilizing these tools and methods, and the COVID-19 pandemic further accelerated the digitization and technological innovation of MFIs.

Through MicroVest’s global network of MFI relationships, we have a unique perspective on how this dynamic is evolving and where it can have the greatest impact for end borrowers and their communities.

Software and data can play a significant role in reducing barriers to financial products for low-income households and SMEs. More traditional MFIs have been inspired to adopt many positive attributes of Fintech start-ups, like user-friendly interfaces, automated processes, innovative data usage, and digital distribution channels. These elements will continue to be important, regardless of whether a lender identifies as a Fintech company. MFIs are also increasingly hiring in-house development teams to build their own products or digitize existing products in ways that would be indistinguishable from a Fintech start-up.

In India for example, Annapurna Finance, a microfinance organization serving over 2.3 million clients, introduced an in-house Geospatial Information System (GIS) that generates and analyzes data using interactive maps and spatial analysis of rural communities where its borrowers reside and work. The GIS team at Annapurna is an essential part of the company, producing analysis that informs decisions on risk management and operations, and building automated tools to widely disseminate data and analytics throughout the organization. With this tool, Annapurna can simulate the impact of a cyclone on a specific group of borrowers, allowing management to proactively identify interventions or products that would help minimize the financial disruption to clients while also preserving the value of Annapurna’s lending portfolio.

In Cambodia, microfinance institution LOLC Cambodia, has developed its own proprietary banking app, iPay. The app is linked to an interest-bearing deposit account that supports KHR, THB, and USD currencies. iPay allows users to access their bank account and view details of their outstanding loans on a 24/7 basis. They can also perform fee-free account transfers, and make everyday payments such as mobile top up and bills.

We see numerous examples of this across our portfolio, with a majority of financial institutions in MicroVest’s portfolio offering some form of digital service to their clients. We anticipate that the utilization of technology will continue to grow in the future. MFIs are increasingly partnering with digital platforms to support distribution or underwriting through tech-enabled systems and processes. Tech-enabled lenders are increasingly seeking the stability and track record that MFIs have established over many years. Digital platforms can offer better data, an agile approach to product development, and proficiency in low-cost digital distribution channels, while microfinance banks with deposit-taking authority have lower funding costs and a deeper understanding of specific industry sectors and communities.

Many Fintechs today are venture capital-backed and have been rewarded with high valuations for showing topline growth, but this often comes at the expense of long-term underwriting performance which can harm borrowers. For some borrowers, taking a loan from a Fintech start-up may have worked out well, as they could often obtain a larger loan amount with less restrictive and time-consuming approval processes. However, these restrictions are intended as safeguards for the borrower. Fintech loans often comes with a trade-off of paying higher interest rates (around 108% per year vs. around 25% per year for MFIs). Fintech-first lenders may also struggle to serve those who are most financially excluded.

Apps designed to run on smartphones may not be accessible to borrowers who cannot afford these devices or live in very rural areas with poor connectivity. Additionally, many borrowers may lack the understanding to comprehend loan terms when they are only presented on the page, without someone to walkthrough of the process or have the opportunity to ask questions. In the worst-case scenario, the pressure to grow can lead Fintechs to make loans that ultimately default, which harms borrowers’ credit scores and results in long-term negative consequences for the borrower. How the microfinance industry builds on these core strengths will be crucial in distinguishing the best-in-class MFIs from the rest in 2023. MicroVest is observing our portfolio of microfinance and SME Finance Institutions continue to innovate. There is still more work to be done—MFIs need to further digitize collections, ensure customer protections are on par with loans originated through traditional channels, and integrate other financial services such as low-cost insurance and savings accounts.

In many cases, these institutions’ knowledge of their customers and communities will guide how to best make use of digital tools. We look forward to a future where, instead of traditional MFIs and Fintechs, financial institutions use software, data and agile processes to build and deliver truly inclusive products at scale.

[1] https://www.safaricom.co.ke/personal/m-pesa/credit-and-savings/m-shwari & https://www.moneymax.ph/personal-loan/articles/tala-loan-philippines

[2] https://microvestfund.com/whats-in-a-microfinance-interest-rate/

DISCLOSURE INFORMATION

The information contained here has been provided by DAI Asset Management, LLC (“DAI-AM”) and no representation or warranty, expressed or implied is made by DAI-AM as to the accuracy or completeness of the information contained herein. Specific portfolio or pipeline companies discussed are for educational purposes only and do not represent all of the portfolio holdings and it should not be assumed that investments in the portfolio or pipeline company identified and discussed were or will be profitable. The companies profiled were selected based on their unique uses of technology in the context of social impact, with no reference to amount of profits or losses, realized or unrealized. The information presented on this page is for informational purposes only and is neither an offer to sell nor a solicitation of an offer to purchase an interest in any DAI-AM product (the “Funds”), and nothing herein should be construed as such. Any such offer or solicitation will be made only by means of delivery of a definitive private offering memorandum which contains a description of the significant risks involved in such an investment. Prospective investors should request a copy of the relevant Memorandum and review all offering materials carefully prior to making an investment.